Terms and Conditions

Procedures to Open a New Account. Federal law requires all banks to obtain, verify, and record information that identifies each person who opens an account in order to help the government fight the funding of terrorism and money laundering activities. When you open an account, we will ask for your name, address, date of birth, and other information to confirm your identity, including your driver’s license or other government issued identification.

Account Agreement. This document, along with any other documents we give you pertaining to your account{s), is a contract that establishes rules which control your account with us. Please read this carefully and retain it for future reference. If you sign a signature card or open an account or continue to use the account, you agree to these rules. You will receive a separate schedule of rates, qualifying balances, and fees if they are not included in this document. If you have any questions, please call us at (833) 887-2265.

This agreement is subject to applicable federal laws, the laws of the state of Mississippi and other applicable rules such as the operating letters of the Federal Reserve Banks and payment processing system rules (except to the extent that this agreement can and does vary such rules or laws). The body of state and federal law that governs our relationship with you, however, is too large and complex to be reproduced here. The purpose of this document is to:

- summarize some laws that apply to common transactions;

- establish rules to cover transactions or events which the law does not regulate;

- establish rules for certain transactions or events which the law regulates but permits variation by agreement; and

- give you disclosures of some of our policies to which you may be entitled or in which you may be

If any provision of this document is found to be unenforceable according to its terms, all remaining provisions will continue in full force and effect. We may permit some variations from our standard agreement, but we must agree to any variation in writing either on the signature card for your account or in some other document. Nothing in this document is intended to vary our duty to act in good faith and with ordinary care when required by law.

As used in this document the words “we,” “our,” and “us” mean the financial institution and the words “you” and “your” mean the account holders and anyone else with the authority to deposit, withdraw, or exercise control over the funds in the account. However, this agreement does not intend, and the terms “you” and “your” should not be interpreted, to expand an individual’s responsibility for an organization’s liability. If this account is owned by a corporation, partnership or other organization, individual liability is determined by the laws generally applicable to that type of organization. The headings in this document are for convenience or reference only and will not govern the interpretation of the provisions. Unless it would be inconsistent to do so, words and phrases used in this document should be construed so the singular includes the plural and the plural includes the singular.

Agreement and Liability. By opening your account, you expressly agree for yourself, and for any person or entity you represent, to these Terms and Conditions and the Fee Schedule in their entirety, including any other documents referenced herein (and thereby incorporated herein in their entirety), as currently stated and as amended from time to time. You authorize us to deduct and fees, without any other prior notice to you, directly from the account balance as accrued. You will pay any additional reasonable charges for services you request which are not covered by this agreement. Each of you also agrees to be jointly and severally {individually) liable for any account shortage resulting from charges or overdrafts, whether caused by you or another with access to this account. This liability is due immediately, and we can deduct any amounts deposited into the account and apply those amounts to the shortage. You have no right to defer payment of this liability, and you are liable regardless of whether you signed the item or benefited from the charge or overdraft. You will be liable for our costs as well as for our reasonable attorneys’ fees, to the extent permitted by law, whether incurred as a result of collection or in any other dispute involving your account. This includes, but is not limited to, disputes between you and another joint account holder, an authorized signer or similar party, or a third party claiming an interest in your account. This also includes any action that you or a third party takes regarding the account that causes us, in good faith, to seek the advice of an attorney, whether or not we become involved in the dispute. You further agree that all costs and attorneys’ fees can be deducted from your account when they are incurred, without notice to you.

Deposits

Generally. Other than cash, we provide temporary provisional deposit credit until collection is final for any items we accept for deposit, including items drawn on Grand Bank. Before settlement of any item becomes final, we act only as your agent, regardless of the form of indorsement or lack of indorsement on the item and even though we provide you provisional credit for the item. We may reverse any provisional credit for items that are lost, stolen, or returned. Unless prohibited by law, we also reserve the right to charge back to your account the amount of any item deposited to your account or cashed for you which was initially paid by the payor bank and which is later returned to us due to an allegedly forged, unauthorized or missing indorsement, claim of alteration, encoding error, counterfeit cashier’s check or other problem which in our judgment justifies reversal of credit. You authorize us to attempt to collect previously returned items without giving you notice, and in attempting to collect we may permit the payor bank to hold an item beyond the midnight deadline. Actual credit for deposits of, or payable in, foreign currency will be at the exchange rate in effect on final collection in U.S. dollars.

We are not responsible for transactions by mail or outside depository until we actually record them. If you deliver a deposit to us and you will not be present when the deposit is counted, you must provide us an itemized list of the deposit (deposit slip). To process the deposit, we will verify and record the deposit, and credit the deposit to the account. If there are any discrepancies between the amounts shown on the itemized list of the deposit and the amount we determine to be the actual deposit, we will notify you of the discrepancy. You will be entitled to credit only for the actual deposit as determined by us, regardless of what is stated on the itemized deposit slip. We will treat and record all transactions received after our “daily cutoff time” on a business day we are open, or received on a day we are not open for business, as if initiated on the next business day that we are open. At our option, we may take an item for collection rather than for deposit. If we accept a third-party check or draft for deposit, we may require any third- party indorsers to verify or guarantee their indorsements, or to indorse in our presence.

Direct Deposits. When you elect for direct deposit of your payroll, pension, and/or government benefits payments, you qualify for 2-Days Early Credit. Access requires our receipt of funds. Deposit availability isn’t guaranteed. Availability can vary by deposit. Transaction limits and risk screenings apply. P2P, checks, e-deposits, and transfers are excluded. We reserve the right to change the 2-Days Early Credit as allowed by law.

Direct Deposits of Benefit Payments. If we are required for any reason to reimburse a federal, state, or local government for all or any portion of a benefit payment that was directly deposited into your account, you authorize us to deduct the amount of our liability to the federal, state, or local government from the account or from any other account you have with us, without prior notice and at any time, except as prohibited by law. We may also use any other legal remedy to recover the amount of our liability.

Withdrawals

Generally. Unless clearly indicated otherwise on the account records, any account holder who signs to open the account or has authority to make withdrawals may, acting alone, withdraw or transfer all or any part of the account balance at any time. Each of account holder authorizes any other account holder who signs or has authority to make withdrawals to indorse any item payable to you or your order for deposit to this account or any other transaction with us.

Postdated checks. Grand Bank does not hold or delay checks from processing, nor does Grand Bank monitor or review dates written upon checks that reflect or indicate postdating of the check. Because we process checks mechanically, postdating is not effective, and we will not be liable for failing to honor any such postdating. Postdating is a matter between you and your check counterparty, and we are not a party to any such postdating agreement.

Checks and withdrawal rules. If you do not purchase your check blanks from us, you must be certain that we approve the check blanks you purchase. We may refuse any withdrawal or transfer request which you attempt on forms not approved by us or by any method we do not specifically permit. We may refuse any withdrawal or transfer request which is greater in number than the frequency permitted by our policy, or which is for an amount greater or less than any withdrawal limitations. We will use the date the transaction is completed by us (as opposed to the date you initiate it) to apply any frequency limitations. In addition, we may place limitations on the account until your identity is verified. Even if we honor a nonconforming request, we are not required to do so later. If you violate the stated transaction limitations (if any), in our discretion we may close your account or reclassify your account as another type of account. If we reclassify your account, your account will be subject to the fees and earnings rules of the new account classification. If we are presented with an item drawn against your account that would be a “substitute check,” as defined by law, but for an error or defect in the item introduced in the substitute check creation process, you agree that we may pay such item.

Cash withdrawals. We recommend you exercise caution when making large cash withdrawals, because carrying large amounts of cash may pose a danger to your personal safety. Instead, you may want to consider a cashier’s check or similar instrument. You assume full responsibility of any loss if cash you withdraw is lost, stolen, or destroyed, and you agree to hold us harmless from any loss you incur as a result of your decision to withdraw funds in the form of cash.

Electronic Check Conversion and Multiple Signatures. Electronic check conversion is a process in which your check is used as a source of information, e.g., the check number, account number, and routing number. The information is then used to make a one-time electronic payment from your account – an electronic fund transfer. The check itself is not the method of payment. In short, electronic check conversion is the process where paper-based check is converted into an electronic transaction at the point-of-sale. Because we are not involved in the conversion process at the point-of-sale, you expressly waive any multiple signature requirements, and you indemnify and hold harmless the bank and its employees, directors, and shareholders regarding any and all damages arising from a violation of any multiple signature requirements.

Notice of withdrawal – We reserve the right to require not less than 7 days’ written notice before each withdrawal from an interest-bearing account, other than a time deposit or demand deposit, or from any other savings deposit as defined by Regulation D. The law requires us to reserve this right, but it is not our general policy to use it. Withdrawals from a time account prior to maturity or prior to any notice period may be restricted and may be subject to penalty. Please refer to the Fee Schedule applicable to your account regarding any penalties.

Overdrafts, Non-sufficient Funds, Balance, Holds

Generally. The information in this section is being provided to help you understand what happens if your account is overdrawn. Understanding the concepts of overdrafts and nonsufficient funds (NSF) is important and can help you avoid being assessed fees or charges. This section also provides contractual terms relating to overdrafts and NSF transactions. An overdrawn account can result in you being charged an overdraft fee or an NSF fee. See the current Fee Schedule. Generally, an overdraft occurs when there is not enough money in your account to pay for a transaction, but we pay (or cover) the transaction anyway. An NSF transaction is slightly different. In an NSF transaction, we do not cover the transaction. Instead, the transaction is rejected and the item or requested payment is returned. In either situation, we can charge you a fee.

Determining your available balance. We use the available balance method to determine whether your account is overdrawn, that is, whether there is enough money in your account to pay for a transaction. Importantly, your available balance may not be the same as your account’s current balance, a/k/a the ledger balance. This means an overdraft or an NSF transaction could occur regardless of your account’s current balance. Your account’s current balance only includes transactions that have settled up to that point in time, that is, deposits and payments that have actually cleared and posted to your account. The current balance does not include outstanding transactions (such as checks that have not yet cleared and electronic transactions that have been authorized but which are still pending). The balance on your periodic statement is the ledger balance for your account as of the statement date.

As the name implies, your available balance is calculated based on the money “available” in your account to make payments. In other words, the available balance takes transactions that have been authorized, but not yet settled, and subtracts them from the current balance. In addition, when calculating your available balance, any “holds” placed on deposits that have not yet cleared are also subtracted from the current balance. For more information on how holds placed on funds in your account can impact your available balance, read the subsection titled “A temporary debit authorization hold affects your account balance.”

Year-to-Date Collected Balance. The Year-to-Date Collected Balance is the actual balance that has been collected in your account in the numerator over the denominator of days the account is open in a year. An example is an account that is opened on 12/1/XX. The Year-to-Date Collected Balance at 12/31/XX will be the collected balance over the 30 days that the account was open for that year. If the account was opened in a prior year, the Year-to-Date Collected Balance would be the average collected balance in the account from January 1st of the current year through the day the computation is made (such as July 10th of the current calendar year).

Collected. When we use the term “collected” when referring to computing your account balance, we are referring the funds for the items that have actually cleared and officially posted to your account.

Overdrafts. You understand that we may, at our discretion, honor withdrawal requests that overdraw your account. However, the fact that we may honor withdrawal requests that overdraw the account balance does not obligate us to do so later. So you can NOT rely on us to pay overdrafts on your account regardless of how frequently or under what circumstances we have paid overdrafts on your account in the past. We can change our practice of paying, or not paying, discretionary overdrafts on your account without notice to you. You can ask us if we have other account services that might be available to you where we commit to paying overdrafts under certain circumstances, such as an overdraft privilege line- of-credit or a plan to sweep funds from another account you have with us. You agree that we may charge fees for overdrafts. We may use subsequent deposits, including direct deposits of social security or other government benefits, to cover such overdrafts and overdraft fees. Overdraft fees are based upon your available balance.

Nonsufficient Funds (NSF) Fees. Grand Bank does not charge NSF Fees at this time.

Balance information. Keeping track of your balance is important, and you can do so via your periodic statement, online banking, our mobile app, calling us, or visiting our branch.

Temporary debit card authorization holds. On debit card purchases, retail merchants may request a temporary hold on your account for a specified sum of money, which may be more than the actual amount of your purchase. This is often called an authorization hold or a pre-authorization hold. When retail merchants make these requests, our processing system cannot determine whether the amount of the hold may exceed the actual amount of your purchase.

Retail merchants may request us to place an authorization hold on your Account for up to 3 calendar days (or for up to 30 business days at the Bank’s discretion for certain types of debit Card transactions, including but not limited to, international car rental and hotel), from the time of the authorization or until the transaction is paid from your Account. However, if the merchant does not submit the transaction for payment within the time allowed, we will release the authorization hold. This means your available balance will increase until the transaction is submitted for payment by the merchant and posted to your Account. If this happens, we must honor the prior authorization, and we will pay the transaction from your Account. In some situations, the amount of the hold may differ from the actual transaction amount since the merchant may not know the total amount you will spend.

Example 1: A restaurant submits the authorization request for the initial cost of your meal before you add a 20% tip.

Example 2: A restaurant submits the authorization request for a rounded number (say, $100 before you sign) but your actual meal costs $78, including tip.

If another transaction is presented for payment in an amount greater than the funds left after the deduction of the authorization hold, that transaction will be considered either (i) a nonsufficient funds (NSF) transaction if we do not pay it or (ii) an overdraft transaction if we do pay it. Grand Bank does not charge NSF fees, but your retail merchant or their financial institution may. Grand Bank may, however, charge an overdraft fee according to our stated policy and the order in which the additional transaction is processed.

Example 1: You have opted-in to our overdraft services for the payment of overdrafts on ATM and everyday debit card transactions, and we subsequently pay an overdraft on your account. Our overdraft fee would be applicable, but we currently do not charge the overdraft fee if: (i) the transaction overdraws the account $10 or less or (ii) if the transaction itself is $10 or less.

Example 2: You have $120 in your account. You swipe your card at the card reader on a gasoline pump. Since it is unclear what the final bill will be, the gas station’s processing system immediately requests a hold on your account in a specified amount, for example, $80. Our processing system authorizes a temporary hold on your account in the amount of $80, and the gas station’s processing system authorizes you to begin pumping gas. You fill your tank and the amount of gasoline you purchased is only $50. Our processing system shows that you have $40 in your account available for other transactions ($120 – $80 =

$40) even though you would have $70 in your account available for other transactions if the amount of the temporary hold was equal to the amount of your purchase ($120 – $50 = $70). Later, another transaction you have authorized is presented for payment from your account in the amount of $60 (this could be a check you have written, another debit card transaction, an ACH debit, or any other kind of payment request). This other transaction is presented before the amount of the temporary hold is adjusted to the amount of your purchase (remember, it may take up to three days for the adjustment to be made). Because the account does not have sufficient funds available to cover the transaction, the transaction will either be (i) returned as NSF or (ii) paid if you have opted into an available overdraft program.

Account Ownership & Beneficiary Designation

Generally. The following rules apply to this account depending on the form of ownership and beneficiary designation, if any, specified on the account records. We make no representations as to the appropriateness or effect of the ownership and beneficiary designations, except as they determine to whom we pay the account funds.

Individual Account – Is an account in the name of one person.

Joint Account With Survivorship. This type of account in the name of two or more persons. Each of you intend that when you die the balance in the account (subject to any previous pledge to which we have agreed) will belong to the survivors. If two or more of you survive, you will own the balance in the account as joint tenants with survivorship and not as tenants in common.

Joint Account Without Survivorship. This type of account is owned by two or more persons. but none of you intend (merely by opening this account) to create any right of survivorship in any other person. We encourage you to agree and tell us in writing of the percentage of the deposit contributed by each of you. This information will not, however, affect the number of signatures necessary for withdrawal.

Revocable Trust or Pay-On-Death Account. If two or more of you create such an account, you own the account jointly with survivorship. Beneficiaries cannot withdraw unless: (i) all persons creating the account die; (ii) the beneficiary is then living; and (iii) we are not otherwise required by Mississippi law to make payment to a parent, custodian, or guardian. If two or more beneficiaries are named and survive the death of all persons creating the account, such beneficiaries will own this account in equal shares, without right of survivorship. The persons creating either of these account types reserves the right to: (i) change beneficiaries; (ii) change account types; and (iii) withdraw all or part of the account funds at any time.

Business, Organization, and Association Accounts. Earnings in the form of interest, dividends, or credits will be paid only on collected funds, unless otherwise provided by law or our policy. You represent that you have the authority to open and conduct business on this account on behalf of the entity. We may require the governing body of the entity opening the account to give us a separate authorization telling us who is authorized to act on its behalf. We will honor the authorization until we actually receive written notice of a change from the governing body of the entity.

Stop Payment Instructions. Unless otherwise provided, the rules in this section cover stopping payment of items such as checks and drafts. Rules for stopping payment of other types of transfers of funds, such as consumer electronic fund transfers, may be established by law or our policy. If we have not disclosed these rules to you elsewhere, you may ask us about those rules.

We may accept an order to stop payment on any item from any one of you. You must make any stop- payment order in the manner required by law and we must receive it in time to give us a reasonable opportunity to act on it before it is presented to us. Because stop-payment orders are handled by computers, to be effective, your stop-payment order must precisely identify the number, date, and amount of the item, and the payee. You may stop payment on any item drawn on your account whether you sign the item or not. Generally, if your stop-payment order is given to us in writing it is effective for six months. Your order will lapse after that time if you do not renew the order in writing before the end of the six-month period. If the original stop-payment order was oral your stop-payment order will lapse after 14 calendar days if you do not confirm your order in writing within that time period. We are not obligated to notify you when a stop-payment order expires. A release of the stop-payment request may be made only by the person who initiated the stop-payment order.

If you stop payment on an item and we incur any damages or expenses because of the stop payment, you agree to indemnify us for those damages or expenses, including attorneys’ fees. You assign to us all rights against the payee or any other holder of the item. You agree to cooperate with us in any legal actions that we may take against such persons. You should be aware that anyone holding the item may be entitled to enforce payment against you despite the stop-payment order.

Additional limitations on our obligation to stop payment are provided by law (e.g., we paid the item in cash or we certified the item). See our Fee Schedule for any applicable fees.

Agreement Amendments & Agreement Termination. We may change any term of this agreement. Rules governing changes in interest rates are provided separately in the Truth-in-Savings disclosure or in another document. For other changes, we will give you reasonable notice in writing or by any other method permitted by law. We may also close this account at any time upon reasonable notice to you and tender of the account balance personally or by mail. Items presented for payment after the account is closed may be dishonored. When you close your account, you are responsible for leaving enough money in the account to cover any outstanding items to be paid from the account. Reasonable notice depends on the circumstances, and in some cases such as when we cannot verify your identity or we suspect fraud, it might be reasonable for us to give you notice after the change or account closure becomes effective. For instance, if we suspect fraudulent activity with respect to your account, we might immediately freeze or close your account and then give you notice. If we have notified you of a change in any term of your account and you continue to have your account after the effective date of the change, you have agreed to the new term(s).

Notices. Any written notice you give us is effective when we actually receive it, and it must be given to us according to the specific delivery instructions provided elsewhere, if any. We must receive it in time to have a reasonable opportunity to act on it. If the notice is regarding a check or other item, you must give us sufficient information to be able to identify the check or item, including the precise check or item number, amount, date and payee. Written notice we give you is effective when it is deposited in the United States Mail with proper postage and addressed to your mailing address we have on file. Notice to any of you is notice to all of you.

Statements. Your duty to report unauthorized signatures, alterations, and forgeries – You must examine your statement of account with “reasonable promptness.” If you discover (or reasonably should have discovered) any unauthorized signatures or alterations, you must promptly notify us of the relevant facts. As between you and us, if you fail to do either of these duties, you will have to either share the loss with us, or bear the loss entirely yourself (depending on whether we used ordinary care and, if not, whether we substantially contributed to the loss). The loss could be not only with respect to items on the statement but other items with unauthorized signatures or alterations by the same wrongdoer.

You agree that the time you have to examine your statement and report to us will depend on the circumstances, but will not, in any circumstance, exceed a total of 30 days from when the statement is first sent or made available to you. You further agree that if you fail to report any unauthorized signatures, alterations or forgeries in your account within 60 days of when we first send or make the statement available, you cannot assert a claim against us on any items in that statement, and as between you and us the loss will be entirely yours. This 60-day limitation is without regard to whether we used ordinary care. The limitation in this paragraph is in addition to that contained in the first paragraph of this section.

Your duty to report other errors or problems – In addition to your duty to review your statements for unauthorized signatures, alterations and forgeries, you agree to examine your statement with reasonable promptness for any other error or problem – such as an encoding error or an unexpected deposit amount.

Also, if you receive or we make available either your items or images of your items, you must examine them for any unauthorized or missing indorsements or any other problems. You agree that the time you have to examine your statement and items and report to us will depend on the circumstances. However, this time period shall not exceed 60 days. Failure to examine your statement and items and report any errors to us within 60 days of when we first send or make the statement available precludes you from asserting a claim against us for any errors on items identified in that statement and as between you and us the loss will be entirely yours.

Errors Relating to EFTs or Substitute Checks. For information on errors relating to electronic fund transfers (e.g., on-line, mobile, debit card or ATM transactions) refer to your Electronic Fund Transfers disclosure and the sections on consumer liability and error resolution. For information on errors relating to a substitute check you received, refer to your disclosure entitled Substitute Checks and Your Rights.

Duty to Notify if Statement Not Received. You agree to immediately notify us if you do not receive your statement by the date you normally expect to receive it. Not receiving your statement in a timely manner is a sign that there may be an issue with your account, e.g., possible fraud or identity theft.

Transfer of Your Account. Ownership of your account may not be transferred or assigned without our prior written consent.

Temporary Account Agreement. If your account documentation indicates that this is a temporary account agreement, each person who signs to open the account or has authority to make withdrawals (except as indicated to the contrary) may transact business on this account. However, we may at some time in the future restrict or prohibit further use of this account if you fail to comply with the requirements we have imposed within a reasonable time.

Setoff. We may (without prior notice and when permitted by law) set off the funds in this account against any due and payable debt any of you owe us now or in the future. If this account is owned by one or more of you as individuals, we may set off any funds in the account against a due and payable debt a partnership owes us now or in the future, to the extent of your liability as a partner for the partnership debt. If your debt arises from a promissory note, then the amount of the due and payable debt will be the full amount we have demanded, as entitled under the terms of the note, and this amount may include any portion of the balance for which we have properly accelerated the due date.

Example 1: Mom and Daughter each have an account with us. Mom’s account is set up as a joint account with Daughter with a right of survivorship. Mom uses the account as her main account. Daughter’s account is similarly set up as a joint account with Mom. Daughter uses the account as her main account. Daughter overdraws her main account and fails to bring it into the positive for 30 days. We contact the Daughter, but she does nothing. After a total of 45 days of the overdraft being left unresolved, we would place a hold on the Mom’s main account because she’s an account holder with the Daughter, and then contact both the Daughter and the Mom. If the account remained overdrawn for 10 days after the notice was mailed, we will offset the Mom’s main account to resolve the Daughter’s overdraft.

Example 2: Joe and Bill own and operate a towing company and a gas station using a single tax identification number. Each of the businesses has a separate bank account but use the same tax identification number. The towing company account becomes overdrawn and remains so for 30 days. We contact both Joe and Bill by phone, but the overdraft remains unresolved. We then send letters to Joe and Bill, but the overdraft remains unresolved. If the account remains overdrawn for 10 days after the notice was mailed, we will offset the gas station account for the amount of the overdraft on the towing company account, because the companies share the same tax identification number.

This right of setoff does not apply to this account if prohibited by law. For example, the right of setoff does not apply to this account if: (i) it is an Individual Retirement Account or similar tax-deferred account; (ii) the debt is created by a consumer credit transaction under a credit card plan (but this does not affect our rights under any consensual security interest); (iii) the debtor’s right of withdrawal only arises in a representative capacity or (iv) setoff is prohibited by the Military Lending Act or its implementing regulations. We will not be liable for the dishonor of any check when the dishonor occurs because we set off a debt against this account. You agree to hold us harmless from any claim arising as a result of our exercise of our right of setoff.

Collection. We may take collection efforts available and allowed under applicable federal and state law in relation to an overdrawn account and/or outstanding balance related to an outstanding balanced owed due to your account becoming overdrawn.

Authorized Signator – Individual Accounts Only. A single individual is the owner. The authorized signer is merely designated to conduct transactions on the owner’s behalf. The owner does not give up any rights to act on the account, and the authorized signer may not in any manner affect the rights of the owner or beneficiaries, if any, other than by withdrawing funds from the account. The owner is responsible for any transactions of the authorized signer. We undertake no obligation to monitor transactions to determine that they are on the owner’s behalf. The owner may terminate the authorization at any time, and the authorization is automatically terminated by the death of the owner. However, we may continue to honor the transactions of the authorized signer until: (a) we have received written notice or have actual knowledge of the termination of authority, and (b) we have a reasonable opportunity to act on that notice or knowledge. We may refuse to accept the designation of an authorized signer.

Restrictive Legends or Indorsements. The automated processing of the large volume of checks we receive prevents us from inspecting or looking for restrictive legends, restrictive indorsements or other special instructions on every check. For this reason, we are not required to honor any restrictive legend or indorsement or other special instruction placed on checks you write unless we have agreed in writing to the restriction or instruction. Unless we have agreed in writing, we are not responsible for any losses, claims, damages, or expenses that result from your placement of these restrictions or instructions on your checks. Examples of restrictive legends placed on checks are “must be presented within 90 days” or “not valid for more than $1,000.00.” The payee’s signature accompanied by the words “for deposit only” is an example of a restrictive indorsement.

Facsimile Signature. We have no obligation to honor facsimile signatures on your checks or other drafts or orders unless you make advance arrangements with us. If we do agree to honor items containing facsimile signatures, you authorize us to charge you at any time for all checks, drafts, or other orders, for the payment of money, that are drawn on us. You give us this authority regardless of by whom or by what means the facsimile signature may have been affixed, so long as they resemble the facsimile signature specimen filed with us and contain the required number of signatures for this purpose. You must notify us at once if you suspect that your facsimile signature is being or has been misused.

Check Processing. We process items mechanically by relying solely on the information encoded in magnetic ink along the bottom of the items. This means that we do not individually examine all of your items to determine if the item is properly completed, signed and indorsed or to determine if it contains any information other than what is encoded in magnetic ink. You agree that we have exercised ordinary care if our automated processing is consistent with general banking practice, even though we do not inspect each item.

Because we do not inspect each item, if you write a check to multiple payees, we can properly pay the check regardless of the number of indorsements unless you notify us in writing that the check requires multiple indorsements. We must receive the notice in time for us to have a reasonable opportunity to act on it, and you must tell us the precise date of the check, amount, check number and payee. We are not responsible for any unauthorized signature or alteration that would not be identified by a reasonable inspection of the item. Using an automated process helps us keep costs down for you and all account holders.

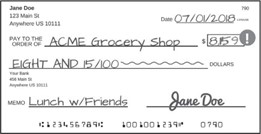

You agree that the amount of the check is based upon the exact amount written in words on the dollar amount line and not the numerical amount written in dollar amount box, as illustrated below:

Check Cashing. We may charge a fee for anyone that does not have an account with us who is cashing a check, draft or other instrument written on your account. We may also require reasonable identification to cash such a check, draft or other instrument. We can decide what identification is reasonable under the circumstances and such identification may be documentary or physical and may include collecting a thumbprint or fingerprint.

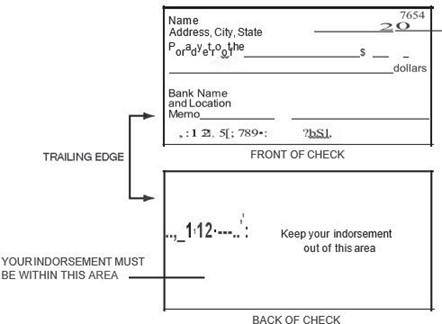

Indorsements. We may accept for deposit any item payable to you or your order, even if they are not indorsed by you. We may give cash back to any one of you. We may supply any missing indorsement(s) for any item we accept for deposit or collection, and you warrant that all indorsements are genuine. To ensure that your check or share draft is processed without delay, you must indorse it (sign it on the back) in a specific area. Your entire indorsement (whether a signature or a stamp) along with any other indorsement information, e.g. additional indorsements, ID information, and driver’s license number, must fall within 1½” of the “trailing edge” of a check. lndorsements must be made in blue or black ink, so that they are readable by automated check processing equipment. As you look at the front of a check, the “trailing edge” is the left edge. When you flip the check over, be sure to keep all indorsement information within 1½” of that edge.

It is important that you confine the indorsement information to this area since the remaining blank space will be used by others in the processing of the check to place additional needed indorsements and information. You agree that you will indemnify, defend, and hold us harmless for any loss, liability, damage or expense that occurs because your indorsement, another indorsement or information you have printed on the back of the check obscures our indorsement. These indorsement guidelines apply to both personal and business checks. DEATH OR INCOMPETENCE – You agree to notify us promptly if any person with a right to withdraw funds from your account(s) dies or is adjudicated (determined by the appropriate official) incompetent. We may continue to honor your checks, items, and instructions until: (a) we know of your death or adjudication of incompetence, and (b) we have had a reasonable opportunity to act on that knowledge. You agree that we may pay or certify checks drawn on or before the date of death or adjudication of incompetence for up to ten (10) days after your death or adjudication of incompetence unless ordered to stop payment by someone claiming an interest in the account.

Fiduciary Accounts. Accounts may be opened by a person acting in a fiduciary capacity. A fiduciary is someone who is appointed to act on behalf of and for the benefit of another. We are not responsible for the actions of a fiduciary, including the misuse of funds. This account may be opened and maintained by a person or persons named as a trustee under a written trust agreement, or as executors, administrators, or conservators under court orders. You understand that by merely opening such an account, we are not acting in the capacity of a trustee in connection with the trust nor do we undertake any obligation to monitor or enforce the terms of the trust or letters.

Credit Verification. You agree that we may verify, and you authorize us to verify as needed, your credit, deposit account, and employment history by any necessary means, including our ordering and receipt of a credit report or deposit account report prepared by a credit reporting agency. We may also verify your credit references and other information you that you provide to us. We may obtain updated or additional information about you, including consumer reports, from time to time for any legitimate purpose including, but not limited to, the extension of credit to you or the review or collection of your Account. We may report late payments, missed payments, or other defaults on your Account to credit reporting agencies.

Legal Actions Affecting Your Account. If we are served with a subpoena, restraining order, writ of attachment or execution, levy, garnishment, search warrant, or similar order relating to your account (collectively “legal action”), we will comply with that legal action. Or, in our discretion, we may freeze the assets in the account and not allow any payments out of the account until a final court determination regarding the legal action. We may do these things even if the legal action involves less than all of you. In these cases, we will not have any liability to you if there are insufficient funds to pay your items because we have withdrawn funds from your account or in any way restricted access to your funds in accordance with the legal action. Any fees or expenses we incur in responding to any legal action, including without limitation, attorneys’ fees and our internal expenses, may be charged against your account. The list of fees applicable to your account provided elsewhere may specify additional fees that we may charge for certain legal actions.

Account Security. You agree that it is your duty and responsibility to protect the account numbers and electronic access devices, e.g., ATM card and Debit Card, that we provide you for your account. Do not discuss, compare, or share information about your account number, PIN, or access credentials with anyone unless you are willing to give them full use of your money. An account number can be used by thieves to issue an electronic debit or to encode your number on a false demand draft which looks like and functions like an authorized check. If you furnish your access device and grant actual authority to make transfers to another person, e.g., a family member or coworker, who then exceeds that authority, you are liable for the transfers unless we have been notified that transfers by that person are no longer authorized. Your account number can also be used to electronically remove money from your account, and payment can be made from your account even though you did not contact us directly and order the payment. You must also take precaution in safeguarding your blank checks. Notify us at once if you believe your checks have been lost or stolen. As between you and us, if you are negligent in safeguarding your checks, you must bear the loss entirely yourself or share the loss with us (we may have to share some of the loss if we failed to use ordinary care and if we substantially contributed to the loss).

Positive Pay and Other Fraud Prevention Services. Except for consumer electronic fund transfers subject to Regulation E, you agree that if we offer you services appropriate for your account to help identify and limit fraud or other unauthorized transactions against your account, such as positive pay or commercially reasonable security procedures, and you reject those services, you will be responsible for any fraudulent or unauthorized transactions which could have been prevented by the services we offered, unless we acted in bad faith or to the extent our negligence contributed to the loss. You will not be responsible for such transactions if we acted in bad faith or to the extent our negligence contributed to the loss. Such services include positive pay or commercially reasonable security procedures. If we offered you a commercially reasonable security procedure which you reject, you agree that you are responsible for any payment order, whether authorized or not, that we accept in compliance with an alternative security procedure that you have selected. A positive pay service can help detect and prevent check fraud and is appropriate for account holders that issue a high volume of checks, a lot of checks to the general public, or checks for large dollar amounts.

Telephone Instructions. Unless required by law or we have agreed otherwise in writing, we are not required to act upon your faxed, voice mail, or telephone answering machine instructions.

Monitoring and Recording Telephone Calls and Consent to Receive Communications. We may monitor or record phone calls for security reasons, to maintain a record, and to ensure that you receive courteous and efficient service. You consent in advance to any such recording. We need not remind you of our recording before each phone conversation.

To provide you with the best possible service in our ongoing business relationship for your account we may need to contact you about your account from time to time by telephone, text messaging or email. However, we must first obtain your consent to contact you about your account because we must comply with the consumer protection provisions in the federal Telephone Consumer Protection Act of 1991, CAN- SPAM Act and their related federal regulations and orders issued by the Federal Communications Commission.

- Your consent is limited to this account, and as authorized by applicable law and

- Your consent does not authorize us to contact you for telemarketing purposes, unless you otherwise agreed elsewhere.

With the above understandings, by this Agreement you expressly authorize us to contact you regarding this account throughout its existence using any telephone numbers or email addresses that you have previously provided to us or that you may subsequently provide to us.

This consent is regardless of whether the number we use to contact you is assigned to a landline, a paging service, a cellular wireless service, a specialized mobile radio service, other radio common carrier service or any other service for which you may be charged for the call. You further authorize us to contact you through the use of voice, voice mail and text messaging, including the use of pre-recorded or artificial voice messages and an automated dialing device. If necessary, you may change or remove any of the telephone numbers or email addresses at any time using any reasonable means to notify us.

Claim of Loss. The following rules do not apply to a transaction or claim related to a consumer electronic fund transfer governed by Regulation E, e.g., a debit card transaction, ATM transaction, or other electronic fund transfer, as such transactions are governed by your Payments and Transfers Agreement with the Bank. For other transactions or claims, if you claim a credit or refund because of a forgery, alteration, or any other unauthorized withdrawal, you agree to cooperate with us in the investigation of the loss, including giving us an affidavit containing whatever reasonable information we require concerning your account, the transaction, and the circumstances surrounding the loss, and you consent to us receiving a copy of any law enforcement report you make. You will notify law enforcement authorities of any criminal act related to the claim of lost, missing, or stolen checks or unauthorized withdrawals. We will have a reasonable period of time to investigate the facts and circumstances surrounding any claim of loss. Unless we have acted in bad faith, we will not be liable for special or consequential damages, including loss of profits or opportunity, or for attorneys’ fees incurred by you. You agree that you will not waive any rights you have to recover your loss against anyone who is obligated to repay, insure, or otherwise reimburse you for your loss. You will pursue your rights or, at our option, assign them to us so that we may pursue them. Our liability will be reduced by the amount you recover or are entitled to recover from these other sources.

Early Withdrawal Penalties. We may impose early withdrawal penalties on a withdrawal from a time account even if you do not initiate the withdrawal. For instance, the early withdrawal penalty may be imposed if the withdrawal is caused by our setoff against funds in the account or as a result of an attachment or other legal process. We may close your account and impose the early withdrawal penalty on the entire account balance in the event of a partial early withdrawal. See your notice of penalty for early withdrawals for additional information.

Address or Name Changes. You are responsible for notifying us of any change in your address or name. Maintaining your current address and name with us is important to prevent identity theft arising from mis-addressed account statements and notices and in the event your account becomes dormant. Account dormancy subjects your account assets to escheatment (transfer) to a state agency in accordance with federal and state law. This Agreement fully incorporates our Unclaimed Property and Escheatment Procedures as if fully written herein.

UTMA Accounts. Accounts subject to the Uniform Transfers to Minors Act are owned by the child, and the child has unconditional use of the account when the child reaches the age of majority. Before the child reaches the age of majority, the account may be accessed only by an authorized custodian, and the funds must be used for the sole benefit of the child. We, however, have no duty or agreement whatsoever to monitor or insure that the acts of a custodian are solely for the benefit of the child. We are not responsible to monitor age or eligibility for an UTMA account, even though our records may include the minor’s date of birth. It is the responsibility of the custodian to properly distribute the funds in the account upon the death of the minor or upon the child reaching the age of majority. For this type of account, the child’s SSN/TIN is used for the Backup Withholding Certification.

Truncation, Substitute Checks, and Other Check Images. If you truncate an original check and create a substitute check, or other paper or electronic image of the original check, you warrant that no one will be asked to make payment on the original check, a substitute check, or any other electronic or paper image, if the payment obligation relating to the original check has already been paid. You also warrant that any substitute check you create conforms to the legal requirements and generally accepted specifications for substitute checks. You agree to retain the original check in conformance with our internal policy for retaining original checks. You agree to indemnify us for any loss we may incur as a result of any truncated check transaction you initiate. We can refuse to accept substitute checks that have not previously been warranted by a bank or other financial institution in conformance with the Check 21 Act. Unless specifically stated in a separate agreement between you and us, we do not have to accept any other electronic or paper image of an original check.

Remotely Created Checks. Like any standard check or draft, a remotely created check (sometimes called a telecheck, preauthorized draft or demand draft) is a check or draft that can be used to withdraw money from an account. Unlike a typical check or draft, however, a remotely created check is not issued by the paying bank and does not contain the signature of the account owner (or a signature purported to be the signature of the account owner). In place of a signature, the check usually has a statement that the owner authorized the check or has the owner’s name typed or printed on the signature line. You warrant and agree to the following for every remotely created check we receive from you for deposit or collection: (1) you have received express and verifiable authorization to create the check in the amount and to the payee that appears on the check; (2) you will maintain proof of the authorization for at least 2 years from the date of the authorization, and supply us the proof if we ask; and (3) if a check is returned you owe us the amount of the check, regardless of when the check is returned. We may take funds from your account to pay the amount you owe us, and if there are insufficient funds in your account, you still owe us the remaining balance.

Unlawful Internet Gambling Notice. You are prohibited to process restricted transactions (as defined in Regulation GG) through this account or your banking relationship with us. Restricted transactions generally include, but are not limited to, credit, electronic fund transfers, checks, or drafts knowingly accepted by gambling businesses in connection with the participation by others in unlawful Internet gambling.

Administrative Holds. We may place an administrative hold on the funds in your account, e.g., refuse payment or withdrawal of funds, if it becomes subject to a claim adverse to: (i) your own interest; (ii) others claiming an interest as survivors or beneficiaries of your account; or (iii) a claim arising by operation of law. The hold may be placed for such period of time as we believe reasonably necessary to allow a legal proceeding to determine the merits of the claim or until we receive evidence satisfactory to us that the dispute has been resolved. We will not be liable for any items that are dishonored as a consequence of placing a hold on funds in your account for these reasons.

Waiver of Notices. To the extent permitted by law, you expressly waive any notice of non-payment, dishonor, or protest regarding any items credited to or charged against your account. For example, if you deposit an item and it is returned unpaid or we receive a notice of nonpayment, we do not have to notify you unless required by federal law.

ACH and Wire Transfers. This agreement is subject to Article 4A of the Uniform Commercial Code – Fund Transfers as adopted in the state in which you have your account with us. If you originate a fund transfer and you identify by name and number a beneficiary financial institution, an intermediary financial institution or a beneficiary, we and every receiving or beneficiary financial institution may rely on the identifying number to make payment. We may rely on the number even if it identifies a financial institution, person or account other than the one named. You agree to be bound by automated clearing house association rules. These rules provide, among other things, that payments made to you, or originated by you, are provisional until final settlement is made through a Federal Reserve Bank or payment is otherwise made as provided in Article 4A-403(a) of the Uniform Commercial Code. If we do not receive such payment, we are entitled to a refund from you in the amount credited to your account and the party originating such payment will not be considered to have paid the amount so credited. Credit entries may be

Notice of Negative Information. Federal law requires us to provide the following notice to customers before any “negative information” may be furnished to a nationwide consumer reporting agency. “Negative information” includes information concerning delinquencies, overdrafts or any form of default. This notice does not mean that we will be reporting such information about you, only that we may report such information about customers that have not done what they are required to do under our agreement. After providing this notice, additional negative information may be submitted without providing another notice. We may report information about your account to credit bureaus. Late payments, missed payments, or other defaults on your account may be reflected in your credit report.

Electronic Funds Transfers/Your Rights and Responsibilities

All EFT transfers are subject to this Terms and Conditions Agreement and our Payments and Transfers Agreement with you, which is fully incorporated into this Agreement as if fully written herein. Please carefully read and retain this Agreement and the Payments and Transfers Agreement as they inform you of your rights and responsibilities regarding your account and EFT transactions.

Electronic Fund Transfer (EFT) Initiated By Third Parties. All EFT transfers are subject to our Payments and Transfers Agreement with you. You may authorize a third party to initiate an EFT between your account and the third party’s account but do so only with persons you personally know and trust. EFT transfers are irreversible, and the EFT may be a one-time occurrence or recurring transaction. These transfers may use the Automated Clearing House (ACH) or other payments network. Your authorization to the third party to make these transfers can occur in a number of ways. For example, your authorization to convert a check to an EFT or to electronically pay a returned check charge can occur when a merchant provides you with notice and you go forward with the transaction {typically, at the point of purchase, a merchant will post a sign and print the notice on a receipt). In all cases, these third-party transfers will require you to provide the third party with your account number and bank information. This information can be found on your check as well as on a deposit or withdrawal slip. Thus, you should only provide your bank and account information {whether over the phone, the Internet, or via some other method) to trusted third parties whom you have authorized to initiate these electronic fund transfers. Examples of these transfers include, but are not limited to:

- Preauthorized You may make arrangements for certain direct deposits to be accepted into your checking or savings account.

- Preauthorized payments. You may make arrangements to pay certain recurring bills from your checking or savings account.

- Electronic check conversion. You may authorize a merchant or other payee to make a one-time electronic payment from your checking account using information from your check to pay for purchases or pay bills.

- Electronic returned check charge. You may authorize a merchant or other payee to initiate an electronic funds transfer to collect a charge in the event a check is returned for insufficient

Please also see Limitations on frequency of transfers section regarding limitations that apply to savings accounts.

24-Hour Telephone Transfers. You may access your account by telephone 24 hours a day at (800) 695- 3197 using your PIN, a touch tone phone, and your account numbers to:

- transfer funds from your checking account to another checking or savings account

- transfer funds from your savings account to another savings or checking account

- make payments on your loan with us using your checking account

- make Bill Pay payments from your checking account to third parties

- get the account balance of your checking or savings account

Please also see Limitations on Frequency of Transfers section regarding limitations that apply to telephone transfers.

ATM Transactions. You may access your account by ATM using your ATM Card or Debit Card and PIN to:

- make deposits to your checking or savings account;

- withdraw cash from your checking or savings account (See your Fee Schedule for any Grand Bank fees. Be aware non-Grand Bank ATM fees may apply);

- transfer funds from your checking or savings account to another checking to savings account; or

- get information about the account balance of your checking or savings account

Some of these services may not be available at all ATM terminals. See your Fee Schedule for any transaction size or frequency limitations.

Debit Card POS Transactions. You may access your checking account to purchase goods or services in person, online, or by phone, or get cash from a merchant (if the merchant so permits) or a participating bank ATM and do anything that a participating merchant will accept.

Currency Conversion and International Transactions. When you use your Debit Card at a merchant that settles in currency other than US dollars, the charge will be converted into the US dollar amount. The currency conversion rate used to determine the transaction amount in US dollars is either a rate selected by the payment processor from the range of rates available in wholesale currency markets for the applicable central processing date, which rate may vary from the rate the processor itself receives, or the government-mandated rate in effect for the applicable central processing date. The conversion rate in effect on the processing date may differ from the rate in effect on the transaction date or posting date. If the payment processor charges us international transaction fees, then we will pass those fees on to you. An international transaction is a transaction where the country of the merchant is outside the USA.

Advisory Against Illegal Use. You agree not to use your ATM or Debit Card for illegal gambling or other illegal purpose. The online display of payment card logo by an online merchant does not necessarily mean that transactions with that merchant are lawful in all jurisdictions.

Online and Mobile Banking Transfers. You may access your account through: (i) the internet using your computer by logging onto our website at www.grand.bank; or (ii) by downloading our mobile app and using your password and access ID, to:

- transfer funds from your checking account to another checking or savings account

- transfer funds from your savings account to another savings or checking account

- make payments on your loan with us using your checking account

- make Bill Pay payments from your checking account to third parties

- get the account balance of your checking or savings account

Our website and mobile app terms and conditions are fully incorporated within this Agreement as if fully written herein. You may be charged access fees by your cell phone provider based on your individual plan. Web access is needed to use this service. Check with your cell phone provider for details on specific fees and charges. Please also see the Limitations on Frequency of Transfers section regarding limitations that apply to online and mobile transfers, which is found in our Payments and Transfers Policy.

Mobile Remote Deposit Capture (RDC) Service. We offer RDC as part of our Mobile Banking Service. RDC allows you to deposit personal checks, certified checks, bank counter checks, and bank official checks made payable to you into your checking account using your wireless device by scanning the check and transmitting to us the image of the check and the data it contains. You can use your wireless device to make a deposit from anywhere at any time, subject to your carrier’s coverage limitations. You acknowledge and agree that an RDC is not an electronic fund transfer as that term defined in federal Regulation E.

The Bank makes no warranties that RDC will be error free, secure, and uninterrupted, and you agree that your use of RDC is at your own risk and on an “as is” basis. We reserve the right to deny your access to RDC without prior notice if we are unable to confirm your authority to access RDC or we believe a denial is necessary for security reasons.

RDC accepts checks made payable to you that are drawn on a U.S. bank. RDC does not accept checks payable to others or to a business, nor travelers cheques, money orders, foreign checks, substitute checks, returned checks, postdated checks, or stale-dated checks more than 6 months old. RDC deposits are limited to one check per deposit and subject to the daily deposit limit set forth in the Fee Schedule. You must indorse the check on the back with your signature and print “For Mobile Remote Deposit Only” below your signature. All deposits are subject to verification and can be adjusted upon review.

Limitations on Savings Account Transfers. You are limited to a maximum of six (6) transfers per monthly statement from any type of savings account to any other account or third party via telephone, online access, mobile access, preauthorized agreement, or by check, draft, or similar order. The first three (3) such transfers are free, but fees are assessed for any further transfers. Please refer to your Fee Schedule. Savings accounts with excessive transfer activity may be converted to a transaction deposit account.

Charges or Fees. We do not assess charges or fees for direct deposits to any type of account, nor for preauthorized payments from any type of account. Except as indicated elsewhere, we do not charge for these electronic fund transfers.

ATM Operator/Network Fees. When you use an ATM not owned by us, you may be charged a fee by the ATM operator or any network used, and you may be charged a fee for a balance inquiry even if you do not complete a fund transfer.

Transaction Documentation

- Terminal You should be able to obtain a receipt when making a transfer to or from your account using an ATM or POS terminal, unless the amount of the transfer is $15 or less.

- Preauthorized You can call us at (855) 288-2265 to confirm whether direct deposits were made to your account from the same person or company. We do not provide you proactive notice of the success or failure of a direct deposit.

- Periodic statements. You will get a monthly account statement from us for your checking and savings accounts.

Stop Preauthorized Payments. If you have authorized us in writing to make regular payments out of your account, you can stop any of these payments by calling or writing us at the telephone number or address listed in this disclosure in time for us to receive your request at least 3 business days or more before the payment is scheduled to be made. If you call, we may also require you to put your request in writing and get it to us within 14 days after you call. If you order us to stop one of these payments at least 3 business days or more before the transfer is scheduled, and we do not do so, we will be liable for your losses or damages. Please refer to our separate fee schedule for the amount we will charge you for each stop- payment order you give.

Preauthorized Payment Notice of Varying Amount. If the previously authorized automatic payment amount will need to change, the recipient payee must give you 10-day prior written notice of when the change will occur and much will be the new payment. For instance, your monthly mortgage payment may increase if your property tax increased and you have an escrow account for property taxes. In the alternative, you may choose to receive notice only when the payment would differ by more than a certain amount or when the amount would fall outside dollar limits that you set.

Liability of the Bank for Failure to Make Transfers. If we do not complete a transfer to or from your account on time or in the correct amount according to our agreement with you, we will be liable for your losses or damages, except when:

- If, through no fault of ours, you do not have enough money in your account to make the

- If you have an overdraft line and the transfer would go over the credit

- If the ATM where you are making the transfer does not have enough

- If the ATM or system was not working properly and you knew about the breakdown when you started the transfer.

- If circumstances beyond our E.g., fire or flood, prevent the transfer, despite reasonable precautions that we have taken.

- Other exceptions stated in our agreement with

Confidentiality. We will disclose information to third parties about your account or the transfers you make: (i) where it is necessary for completing transfers; or (ii) in order to verify the existence and condition of your account for a third party, such as a credit reporting agency or merchant; or (iii) in order to comply with government agency or court orders; or (iv) as explained in our Privacy Policy, which is fully incorporated within this Agreement as if fully written herein.

Unauthorized Transfers or Theft. If you suspect that an unauthorized electronic funds transfer has occurred on your account, or if you suspect your card, code, CVC, or PIN has been lost, stolen, or compromised, CALL US IMMEDIATELY at (833) 887-2265 during business hours or call our 24-hour hotline at (800) 554-8969. If you notify us within two business days after learning of the unauthorized transfer, loss, theft, or compromise, then your liability is limited to the lesser of $50 or the amount of unauthorized transfers or transactions that occurred BEFORE you gave us notice. If you fail to notify us within two business days after learning of the unauthorized transfers or transactions, then your liability can increase up to $500.

Periodic Statement 60-day rule. If you fail to notify us within 60 days of the mailing date of your statement that an unauthorized transfer or transaction occurred, then you may not get back any money you lost after the 60 days if we can prove that we could have stopped someone from taking the money if you had told us in time. If a good reason kept you from telling us, such as a hospital stay, we may extend the time period in our discretion.

Statement Errors Resolution Notice. If your monthly statement contains unauthorized transfers, transactions, or errors, YOU MUST notify us within 60 days of the mailing date of your statement by phone or in writing and provide the following information:

- Your name and account number

- Identify the unauthorized transfer, transactions, or error on your statement

- Tell us the dollar amount of the unauthorized transfer, transaction, or error

- Provide us the basis of your dispute

If you contact us by phone, we may require that you mail us your dispute in writing within 10 business days. Write or call us at Grand Bank for Savings, FSB, Deposit Operations, P.O. BOX 16988, Hattiesburg, MS 39404, (833) 887-2265. We are open Monday through Friday, excluding Saturdays, Sundays, and federal holidays.

We will determine whether an error occurred within 10 business days after we hear from you and will correct any error promptly. If we need more time, however, we may take up to 45 days (90 days if the transfer involved a new account, a point-of-sale transaction, or a foreign-initiated transfer) to investigate your complaint or question. If we decide to do this, we will credit your account within 10 business days for the amount you think is in error, so that you will have the use of the money during the time it takes us to complete our investigation. If we ask you to put your complaint or question in writing and we do not receive it within 10 business days, we may not credit your account. Your account is considered a new account for the first 30 days after the first deposit is made, unless each of you already has an established account with us before this account is opened.

We will mail you the results of our review within three business days after completing our investigation. If we decide that there was no error, we will send you a written explanation. You may ask for copies of the documents that we used in our investigation.

NOTICE OF ATM/NIGHT DEPOSIT FACILITY USER PRECAUTIONS. As with all financial transactions, please exercise discretion when using an automated teller machine (ATM) or night deposit facility. For your own safety, be careful. The following suggestions may be helpful.

- Prepare for your transactions at home (for instance, by filling out a deposit slip) to minimize your time at the ATM or night deposit facility.

- Mark each transaction in your account record, but not while at the ATM or night deposit facility. Always save your ATM receipts. Don’t leave them at the ATM or night deposit facility because they may contain important account information.

- Compare your records with the account statements or account histories that you

- Don’t lend your ATM card to

- Remember, do not leave your card at the ATM. Do not leave any documents at a night deposit

- Protect the secrecy of your Personal Identification Number (PIN). Protect your ATM card as though it were cash. Don’t tell anyone your PIN. Don’t give anyone information regarding your ATM card or PIN over the Never enter your PIN in any ATM that does not look genuine, has been modified, has a suspicious device attached, or is operating in a suspicious manner. Don’t write your PIN where it can be discovered. For example, don’t keep a note of your PIN in your wallet or purse.

- Prevent others from seeing you enter your PIN by using your body to shield their

- If you lose your ATM card or if it is stolen, promptly notify us. You should consult the other disclosures you have received about electronic fund transfers for additional information about what to do if your card is lost or stolen.

- When you make a transaction, be aware of your surroundings. Look out for suspicious activity near the ATM or night deposit facility, particularly if it is after sunset. At night, be sure that the facility (including the parking area and walkways) is well lighted. Consider having someone accompany you when you use the facility, especially after If you observe any problem, go to another ATM or night deposit facility.

- Don’t accept assistance from anyone you don’t know when using an ATM or night deposit

- If you notice anything suspicious or if any other problem arises after you have begun an ATM transaction, you may want to cancel the transaction, pocket your card and leave. You might consider using another ATM or coming back later.

- Please be sure to close any entry door completely upon entering and exiting the ATM or night depository facility.

- Do not permit any unknown persons to enter the facility after regular banking

- Don’t display your cash; pocket it as soon as the ATM transaction is completed and count the cash later when you are in the safety of your own car, home, or other secure surrounding.

- At a drive-up facility, make sure all the car doors are locked and all of the windows are rolled up, except the driver’s window. Keep the engine running and remain alert to your surroundings.

- We want the ATM and night deposit facility to be safe and convenient for Therefore, please tell us if you know of any problem with a facility. For instance, let us know if a light is not working or there is any damage to a facility. Please report any suspicious activity or crimes to both the operator of the facility and the local law enforcement officials immediately.

Funds Availability for Cash Deposits. If you deposit cash funds in person with an employee of our physical branch in Hattiesburg, MS, then the funds will be available for withdrawal not later than the business day after the banking day on which the cash is deposited. If you deposit cash, but not in person with an employee of our physical branch in Hattiesburg, MS, such as at our network ATM or at our retail store agent, then the funds will be available for withdrawal not later than the second business day after the banking day on which the cash is deposited.

Funds Availability for ACH Electronic Deposits. If funds are deposited into your account by ACH electronic deposit, including wires, then the funds will be available for withdrawal not later than the business day after the banking day on which we received the ACH electronic deposit. An ACH electronic deposit is deemed received when we have received both payment in actually and finally collected funds and information on the account and the amount to be credited.

Funds Availability for Checks Deposited in Person. If you deposit a certain check in person with an employee of our physical branch in Hattiesburg, MS, then the funds will be available for withdrawal not later than the business day after the banking day on which the cash is deposited. Such a certain check must be deposited in an account held by a payee of the check or money order, and is limited to the following:

- A S. Treasury check;

- A S. Postal Service money order;

- A check drawn on a Federal Reserve Bank or Federal Home Loan Bank;

- A check drawn by a state or a unit of general local government; and

- A cashier’s, certified, or teller’s check;

For all other checks deposited in person with an employee of our physical branch in Hattiesburg, MS, then the funds will be available for withdrawal as follows:

The lesser of $225 or the aggregate amount deposited on any one banking day to all accounts of the customer by check or checks not subject to next-day availability under paragraphs (c)(1) (i) through (vi) of this section.

Funds Availability for Remote Deposit Checks. If you deposit a U.S. Treasury check using our remote deposit app on your mobile device into an account held by a payee of the check, then the funds will be available for withdrawal not later than the business day after the banking day on which the cash is deposited. If you deposit another certain check or money using our remote deposit app on your mobile device into an account held by a payee of the check or money order, then the funds will be available for withdrawal not later than the second business day after the banking day on which funds are deposited. Such other certain check or money order is limited to the following:

- A S. Postal Service money order;